the MoneySmartLife.org Lifestyle blogEmpowering sustainable financial well-being for working class families

|

|

Holidays are times of gathering for families. As such it provides opportunities to help the extended family strengthen its economic foundation. These are the perfect times to discuss estate plans, elder care, custodial expectations and more. Now that sounds pretty heavy and it may be depending upon how your family views these subjects. But not talking about it isn’t wise.

Normally estate matters are resolved as part of a process that takes time to complete. But they must be started. Start with the easy stuff. Are wills in place for all adults 18 years and older? What happens to the kids? Are there durable power of attorneys and health care directives in place for all adults 18 years and older? It is better to have these discussions before a crisis requires them. Not having proper estate plans in place has put significant stress on family relationships regardless of assets forever. Yours will be no different. Take the next steps depending on what is learned. Help those that have no plan get one written and recorded. Encourage those that have a partial plan to upgrade. Lead by example. Family gatherings can also provide opportunities to save money through the elimination of redundant streaming services expenses. Most streaming services allow for multiple profiles or device logins. Maximizing profiles used for each service and spreading the cost of the subscriptions can expand extended family access while lowering individual unit costs. This is also a time to review subscription services already shared to see if they are still used and eliminate those that aren’t. Some services can be eliminated seasonally depending upon demand. The family can adopt a “binge and go” strategy. This is where a service is subscribed to for a period of time to allow episodes to be binged. The effect is to make the service disposable, use it then lose it. This eliminates autopilot spending that subscriptions require. Here is a list of some popular subscription streaming services and links to their multiple user policies:

0 Comments

Financial shocks are inevitable during a lifetime. “Stuff happens,” according to the PG-rated version of that cliche. When it does, my language is more NC-17. Nevertheless, happen it does. The most common financial shocks for working-class families are:

What is an emergency fund? It is a “liquidity buffer” between you and ruin. If you have very little saved — say $200 to $500 — each additional dollar you set aside dramatically reduces your likelihood of falling into financial hardship. It can be any of these items. Some are decidedly better options than others:

Forget the 3 to 6 months of take-home pay that is commonly parroted throughout financial media and literature. This goal is often unattainable for low-income wage earners. A more realistic minimum target is $2,467. A fund of this amount will be sufficient for most emergencies. Having such a fund stops you from getting stuck with short term remedies with long term consequences like being late on rent or borrowing from a payday lender. Often creating a cycle of cash draining late fees and prolonged financial insecurity. Building an emergency fund is your #1 priority. You should well establish an emergency fund before you divert resources to the very prudent debt reduction strategy necessary for your long term success. You should continue or start making all minimum payments on time and continue to do so until your emergency is well funded. Debt reduction is achieved by consistent application of payment to the principal balance. Having an emergency fund will let you maintain a good payment history so you won’t have to “rob Peter to pay Paul” when the inevitable happens. One missed credit card minimum payment can close off what may be a critical asset during a financial emergency and put a big hole in your safety net. Modified universal default terms may render a late payment to one lender a catastrophe in your creditworthiness regardless of your actual payment history. Your ability to borrow should be viewed as part of your safety net. It creates capacity and demonstrates financial capability. Your credit card cash advances and spending limits are critical components that can help mitigate some of the impacts of an emergency while buying you time. An excellent credit score can give you immediate access to additional money during an emergency. It is a MoneySmartLife strategy to responsibly and proactively expand your borrowing capacity annually. Just as your net worth expands annually, so should your credit capacity. They weave your safety net tighter and softer.

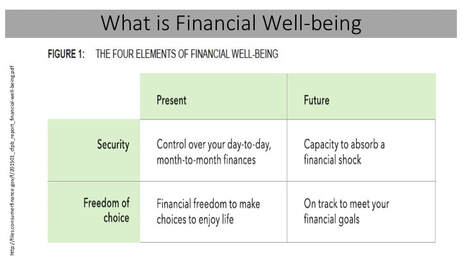

Financial Well-Being Matrix Financial Well-Being Matrix

Recently the weather gave us notice that Nature was about to bring about a season change. Like it or not, ready or not the seasons will change. According to wise King Solomon in Ecclesiastes, everything under heaven has a season.That would include the American and global economies. And importantly, seasons change.

The economy's season is changing. Possible recession, the impact of tariffs on prices, and stagnant wage growth. In the words from HBO's Game of Thrones, "Winter is coming." Part of financial well-being is "the capacity to absorb a financial shock." The key is your CAPACITY. Here are four strategies to do now to increase your capacity.

check out ways to save money this week on our FB feed

Okay the BK is discharged. Now let's start rebuilding your credit score. This not a quick fix. It also assumes you have effectively dealt with whatever caused you declare bankruptcy whether it be situation, lifestyle, or lack of financial capabilities.

This strategy is front-loaded with a long term payoff because of the BK credit restoration timeline. A BK can be on your credit report for up to 10 years. The good news is that its impact lessens on your credit report the further removed it is from the present. You may be eligible for a mortgage or auto loan in much less time if your other factors are strong. Here are the six steps to rebuild a perfect credit score: 1.Be wary of credit repair companies.

2. Start now. Be patient.

4. Check your credit reports 90 days after BK and then at least annually thereafter.

|

Archives

May 2020

Categories

All

|

RSS Feed

RSS Feed