the MoneySmartLife.org Lifestyle blogEmpowering sustainable financial well-being for working class families

|

|

0 Comments

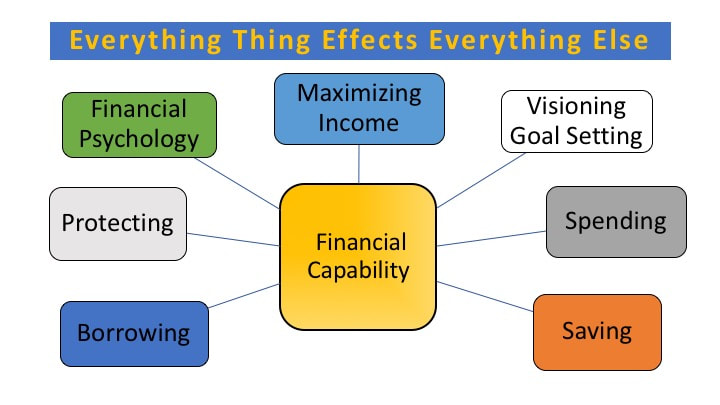

Financial capability is the internal capacity to act in one's best financial interest, given socioeconomic environmental conditions. It therefore encompasses the knowledge, attitudes, skills, and behaviors of consumers with regard to managing their resources and understanding, selecting, and making use of financial services that fit their needs.

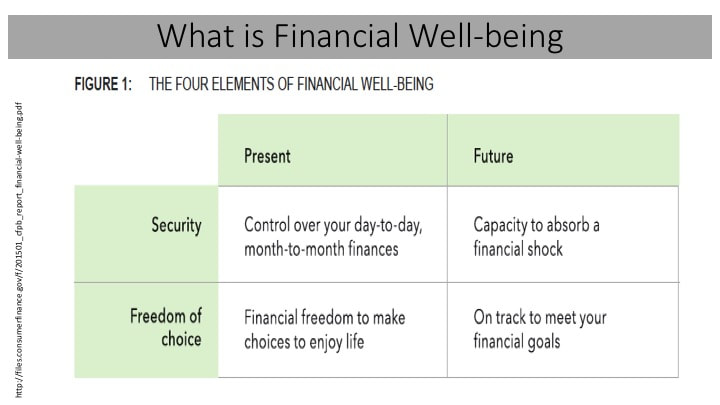

Consumers can experience financial well-being—or a lack of it—regardless of income. It’s a highly personal state, not fully described by objective financial measures. Instead, well-being is defined as having financial security and financial freedom of choice, in the present and in the future.

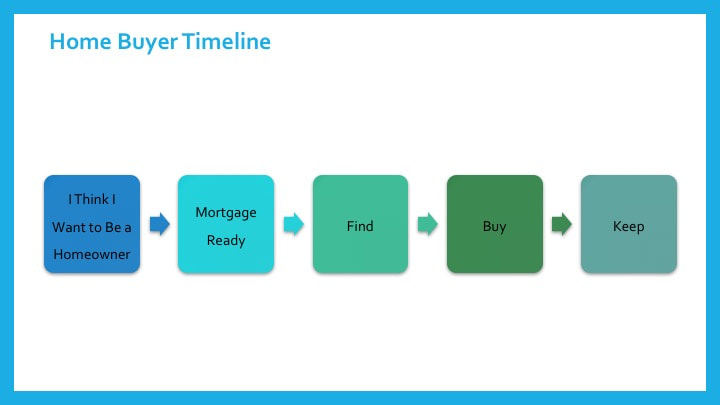

If you are paying credit card interest on consumables like gas, food, entertainment or travel, then you are hustling out of the world backwards. The good memories that linger are often corrupted by payment stress. It is so much better to come back with just the memories and not the bills. Stop paying double digit interest on your contributions to the sewage treatment plant and carbon emissions. Credit card interest rates are usurious compared to other forms of borrowing. Current rates range between 13.12% and 22.99%. Carrying a balance on a credit card is not is good for your money. You can end credit card debt, if you do the right things based on your circumstances. You can start by resolving to use ONLY cash for consumables from now on. Cash limits your spending. It makes your spending more intentional and purpose driven. The key is to not take more cash than you need. Overspending will create budget shortfalls elsewhere. Cash is any of the cash instruments. That would be debit and gift cards (no overdrafts allowed.) A well managed credit card. That is a credit card that has the statement balance paid in full every month by the due date. And of course, actual dollars and coins. Going to cash for consumables may require a behavior change. Behavior change can be hard if you don’t frame it in your mind right. Think of it as a benefit and not a sacrifice. It is you not setting yourself up for failure. It also eliminates committing future earnings to service debt for transient purchases. So go to cash for all consumables going forward. It may be tight for a while. You will use cash to take care of your current fuel, entertainment, and food needs. You will have to service and payoff the current debt, also. Until then you are going to have to find creative ways for your family to conserve, entertain and eat. Some options include short term use of a food bank. Leaving your vehicle parked. Selling some of your stuff. Finding a paying side hustle. Netflix and chill. What are your strategies?  Home ownership is arguably the American dream. Its sometimes nightmarish qualities are often obscured when the "dream" is promoted to novice home buyers. The hugely influential real estate-financial services complex(real estate agents and brokers, banks, mortgage brokers, builders, retailers, and real estate services companies (title, appraisal and inspection) generate huge profits from the first time home buyers. It is in their interest to keep that outlook as rosy as possible. When it comes to buying your home you need to be laser-focused on what your interests are in the transaction. Understanding this will give you confidence and negotiating leverage. Owning a home is more than a notion. Buying a home has a certain degree of difficulty. Keeping a home may be more difficult yet depending on your buying choices. Did you make informed choices based on information provided by non-interested parties? Was the information objective? Were all your options vetted? The assumptions that often go with the homeownership dream are often countered by geo-vulnerability. Not all the traditional assumptions are valid for all neighborhoods. If nothing else your home's real estate is hyper-local, zip code level local.

|

Archives

May 2020

Categories

All

|

RSS Feed

RSS Feed