the MoneySmartLife.org Lifestyle blogEmpowering sustainable financial well-being for working class families

|

|

If you have done some things right and your financial house appears in order, a relative will ask you to co-sign a loan for them. Co-signing is only one of the ways available to help your credit-challenged relative. There are other ways that may deliver the desired results with less exposure and risk for you, especially with a little bit of planning.

Let’s look at your options and so you can make an informed choice about co-signing. When you co-sign you become a JOINT account holder. Each and every member on a joint account agrees to be individually responsible for 100% scheduled repayment of the outstanding debt regardless of the other members' payments or promises. When you co-sign if a payment is missed, your credit score will receive the full negative impact of the late payment. This could be catastrophic if it compounds an already diminished credit score. No doubt, the new co-signed loan’s high-balance-to-limit ratio, and short history have already reduced your credit scores several points. That happened just by signing up; missed payments or not. So be prepared to take a credit score hit when you co-sign. How long will it take your score to recover from these factors assuming a pristine repayment history? The answer depends on several factors. Credit scoring is an art and a science. Whatever calculations the algorithm conjures to determine our scores, the following is empirically factual for every credit score. They go down a helluva lot faster than they rebound. It is never down one month; up the next for any credit scoring model in existence regardless of the previous history. If your relative needs you to co-sign to “build credit” then you can also do that by making them an authorized user on your credit cards. If you do, you will almost immediately transfer your credit history to theirs. And without any risk or exposure to new debt for either of you. Now, this strategy will not work for impulse or emergency “gotta have a co-signer or else “ situations. But adding someone as an authorized user can be the gift that keeps on gifting. As with most successful credit score improvement strategies, the more time you give this one, the better. But the gift isn’t for everyone. Here are six questions whose answers will help you decide if your situation is a fit for the authorized user strategy:

Good credit grandparents can leave good credit legacies safely to multiple generations since there are rarely limits on the number of authorized users. Just make sure that each of the six questions has the right answer.

0 Comments

Everyone can have a great credit score (750+.) How long it takes depends on from where you start. It will take a person with a 450 score longer than a person with 620. And both longer compared to a 720 score. But it can be done. The journey of 1,000 miles begins with the first step. Here are 2 steps to having a great credit score. Step One STOP putting BAD news on your credit report. If you do nothing, your credit will clean itself up in 7 years. The Fair Credit Reporting Act (FCRA) requires that.

Step Two Put some good news on your credit report. Gotta Do It! Current positive tradelines on your credit report have a greater impact on improving your credit score than older negative ones. They will improve your score faster and easier than just doing Step One alone. Here are some ways to put positive tradelines on your credit report.

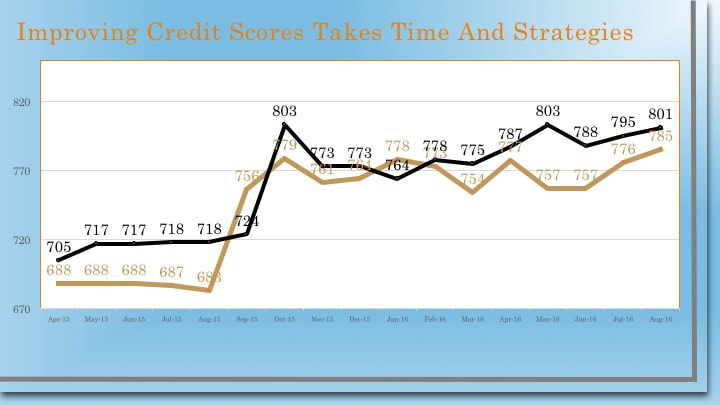

Credit Score improvement Chart Short Answer is that it dies with you IF.....

If you have bad credit be encouraged you can have good credit, if you want it. Having a “prime” credit score can make a significant beneficial difference in your life. Non-prime credit scores will result in limited more expensive borrowing options, if available at all. Borrowing from time to time is a reality and necessity of modern financial life. Short-term borrowing costs impact your long-term financial well-being. Your ability to minimize those costs is based on your financial capability. In this adversarial economic system, you can either "play the game" or "be played by the game." Credit heals itself. If you do nothing on your credit for the next 7 years you will have a clean credit report by law. The only exception would be the 10 years required for a Chapter 7 bankruptcy to clear. But just waiting for the bad news to fall off your report isn’t good enough. You also need to engage the system for your benefit.  Actual Credit Score Improvement Graph  It is difficult to give generalized financial advice. Because everyone’s situation is different and the dollars are in the details. Having said that, here's a look at the benefits of a balance transfer.

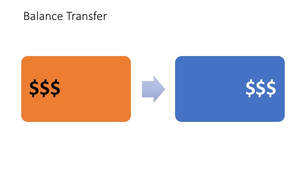

A balance transfer is when you move the debt from one debt instrument to another. In most cases, a credit card is the receiving instrument. Some pros to doing a balance transfer.

Some things you should be aware of when making a balance transfer. |

Archives

May 2020

Categories

All

|

RSS Feed

RSS Feed